The increase in the capital gains inclusion rate could have an impact on your tax bill, even for gains realized before June 25, 2024.

Two months after announcing the increase in the capital gains inclusion rate from one-half to two‑thirds, Finance Canada has released the long-awaited legislative proposals implementing the announcement.

The proposed amendments1 could have unforeseen repercussions on your tax bill, even for gains realized before June 25, 2024.

You should pay particular attention to changes in the capital gains inclusion rate in the following cases:

- You are an individual who will realize more than $250,000 in capital gains in 2024.

- You received a tax-free capital dividend from a corporation with a fiscal year-end on or after June 25, 2024 following the realization of capital gains for a tax year that includes that date.

- You expect to benefit from the increased capital gains deduction in 2024.

- You or your corporation realized a capital gain in a prior year for which a capital gains reserve was deducted from the calculation of income related to amounts not yet collected.

Let’s take a closer look at how the Notice could impact your tax bill.

Proposed amendments

As announced in the 2024 federal budget, these amendments are aimed at increasing the capital gains inclusion rate from one-half to two-thirds for dispositions that occur on or after June 25, 2024. The first $250,000 of capital gains realized annually by an individual will benefit from the one-half inclusion rate. For corporations and trusts (with the exception of graduated rate estates), the new two-thirds inclusion rate applies as of the first dollar of the gain.

In addition, the capital gains deduction will be increased to $1,250,000 for qualifying dispositions occurring after June 24, 2024.

The application of the new rules for tax years beginning before June 24, 2024 and ending after June 25, 2024 will be governed by a series of specific rules (“Transitional Rules”), which are aimed primarily at implementing a weighted average inclusion rate (“Average Rate”). The Transitional Rules and the Average Rate could affect transactions carried out before June 25, 2024.

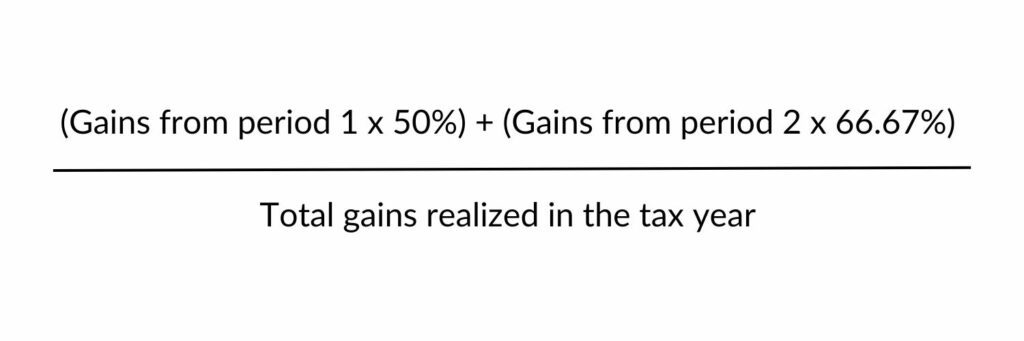

- Calculating the Average Rate

The Transitional Rules and the introduction of the Average Rate apply to all taxpayers. The taxpayer’s tax year will be split into two periods:

- Period 1, which runs from the beginning of the taxpayer’s tax year to June 24, 2024

- Period 2, which runs from June 25, 2024 to the last day of the taxpayer’s tax year

The Average Rate will be calculated as follows:

The calculated Average Rate will apply to all gains realized in the tax year. For example, if a capital gain of $1,000 was realized in period 1 and an additional capital gain of $1,000 was realized in the period 2, the Average Rate for all capital gains for the year would be 58.33%.2

Impact of the Notice on transactions carried out before June 25, 2024

- Capital dividends (tax-free)

The Transitional Rules and the method for calculating the Average Rate could have a major impact on the capital dividends paid in a tax year that includes June 25, 2024, as the Average Rate applies to all capital gains realized in that tax year.

For example, if a corporation with a July 31, 2024 year-end realizes a capital gain of $1,000 on December 31, 2023 and then pays a capital dividend of $500 to its shareholders on January 1, 2024, the realization of a second capital gain of $1,000 on June 30, 2024 will increase its Average Rate for the entire tax year. This would result in an excess capital dividend of $83 on January 1, 2024, when no one could have known that the rate would increase.

If a capital dividend has already been declared, we recommend avoiding realizing capital gains in period 2, or avoiding realizing capital losses in excess of the capital gains from period 1, to avoid unpleasant surprises.

If there is any uncertainty about the realization of capital gains in period 2 of a corporation’s tax year, we recommend exercising caution before paying a dividend from the capital dividend account to avoid creating an excess.

- Capital gains deduction (exemption)

The use of the capital gains deduction, when combined with the Average Rate, could result in a different tax bill than the one anticipated at the time of the budget announcement. Again, gains realized before June 25, 2024 could be taxed at a rate higher than 50%, even if the total capital gains realized after June 25, 2024 are subject to the capital gains deduction.3

Where possible, a sale of qualified small business corporation shares could be considered, making the corporation eligible for the capital gains deduction until 2025. This would prevent the Average Rate from being applied to the portion of gains not subject to the capital gains deduction.

- Capital gains reserves

According to the Notice, a capital gain that has been tax-deferred due to a capital gains reserve deducted from the income calculation for a prior year will be deemed to be realized on the first day of the year, i.e. in period 1. Amounts to be included in the income calculation for subsequent years will be subject to the inclusion rate in effect at that time, i.e. two-thirds.

A taxpayer who can benefit from a capital gains reserve for 2024 might be better off being taxed on the full amount in 2024 rather than benefiting from a capital gains reserve, which would be included in the two-thirds rate in a subsequent year.

It’s therefore worth calculating the advantage of being fully taxed on an amount that could be subject to a reserve when preparing upcoming tax returns.

The decision to accelerate tax payable must be made based on the taxpayer’s particular circumstances, including:

- The type of taxpayer (corporation or individual)

- The amount of the gain in question

- The timing of the realization of capital gains

- The realization of capital losses in period 2 exceeding the amount of the capital gains reserve to be included in income

- The ability to pay the accelerated tax

Additional compliance for personal trusts and partnerships

Although personal trusts are not eligible for inclusion rate relief on the first $250,000 of capital gains, realized gains can be allocated to specific beneficiaries who could benefit from the relief. To ensure the proper treatment of capital gains allocated by a trust or partnership, tax slips issued by trusts and partnerships must properly itemize the realization of gains and losses for each period.

Under certain conditions, the inclusion rate relief benefit can be increased through a trust, thereby optimizing tax planning.

There is still a great deal of uncertainty as to how new rules proposed in the Notice will be applied in practice, as they have not yet been passed by Parliament. We will need to keep a close eye on parliamentary proceedings to see whether these new rules are passed as currently drafted or are amended.

In the meantime, be sure to consult your specialists to properly plan your taxes in light of the proposed amendments, and be vigilant when realizing your capital gains in this transition tax year.

(1) References are made to the Notice of Ways and Means Motion for the introduction of a law to amend the Income Tax Act and the Income Tax Regulations, published by the Honourable Chrystia Freeland, Deputy Prime Minister and Minister of Finance, June 2024, available online (the “Notice”), containing legislative proposals related to the increase in the capital gains inclusion rate from one-half to two-thirds effective June 25, 2024.

(2) ((1,000 $ * 50%) + (1,000 $ * 66.67%))/2,000 $ = 58.33%.

(3) Subject to the 250,000 $ threshold included at 50%.